The second half of 2025 is poised to be a defining chapter in the macroeconomic and Bitcoin market cycles. Fiscal and geopolitical uncertainty have dominated headlines for the first half of 2025. Despite this the U.S. economy continues to experience nominal growth; driven by increasing fiat liquidity, AI-driven productivity gains, and the early effects of Trump-era pro-energy policy.

Core CPI and Global M2 continue to increase. With the fanatical expectation of ‘DOGE’ decreasing the federal budget deficit now in the rearview mirror, the market is embracing the reality that Bitcoiners have been aware of for years: “nothing stops this train.” Financial repression (inflation > interest rates) is not just an “option”, it’s the only item on the menu.

Bitcoin thrives in this environment. With persistently high inflation, the net-producers of society are turning to scarce assets in order to store their wealth. Bitcoin, being the only scarce, neutral, borderless, digital commodity, has emerged as the apex store-of-value asset in a world awash in fiat.

BTC/USD has traded range-bound around $100,000 since early December 2024 but tailwinds are picking up. Q2 was Bitcoin’s highest quarterly close in history, liquidity tides are rising, and the market is gaining a sense of clarity for the first time all year. With all this in mind, we expect Bitcoin to have a breakout performance in the second half of 2025.

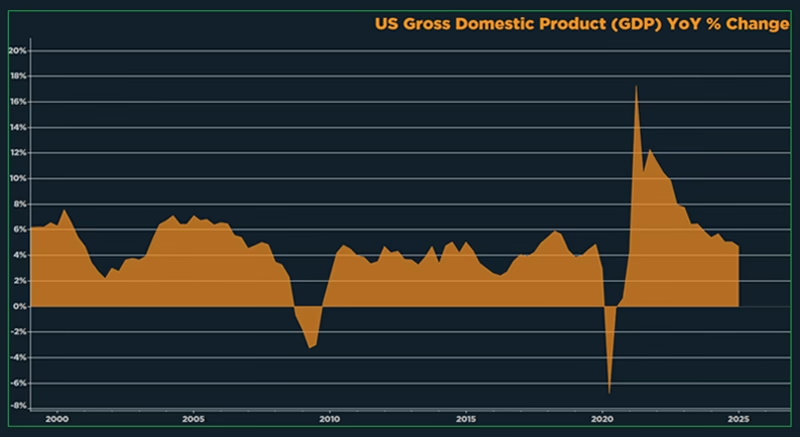

Despite the doom and gloom headlines surrounding tariffs, the U.S. economy is holding strong. In fact, Q3 and Q4 GDP growth are likely to exceed expectations. The reasons are threefold: productivity gains from pro-energy deregulation, loosening financial conditions, and fiscal inertia that continues to inject liquidity into the economy.

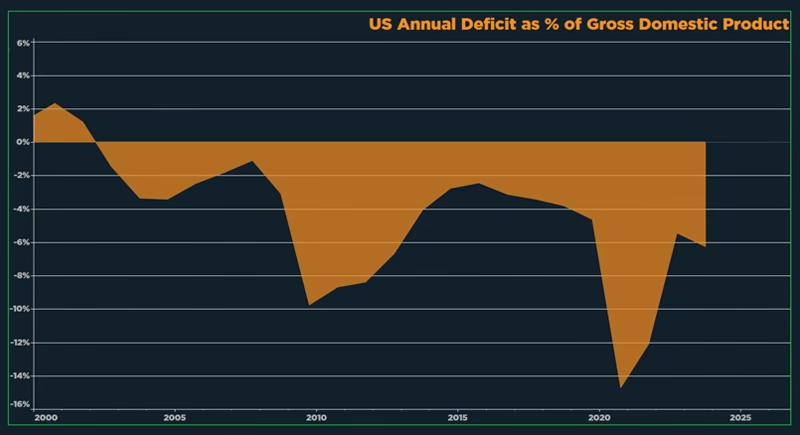

With interest payments on federal debt rising and no meaningful spending cuts on the horizon, the only way for Debt-to-GDP to decline is through growth. Whether that growth takes place organically by the way of AI-driven productivity increases, or the growth comes artificially through monetary debasement, asset prices, specifically Bitcoin, will increase

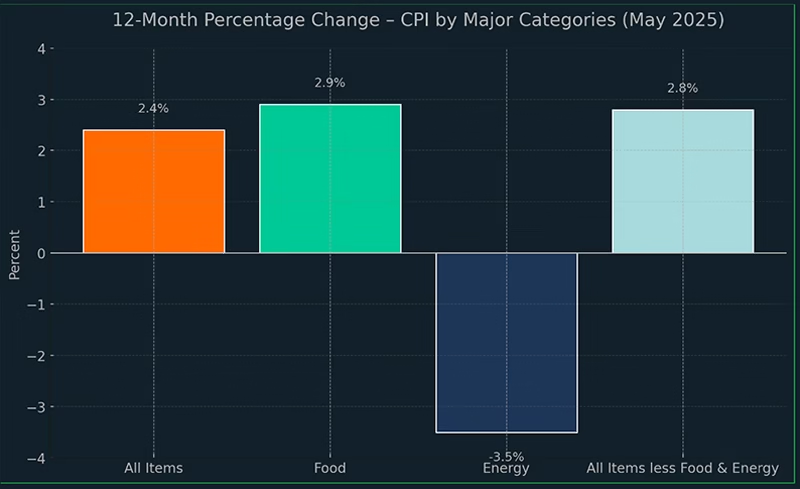

We expect headline CPI to trend lower in late Q3 & Q4, primarily due to increased U.S. energy production driving down the energy component of CPI. This is bullish for US equities as lower energy prices makes inputs cheaper for producers, ultimately leading to more consumer activity. This is great, however, declining CPI values should not be mistaken as declining liquidity. Liquidity is still on the rise (more on that below). Moreover, a decline in CPI does not mean “prices down”, it means “prices up but at a slower rate.”

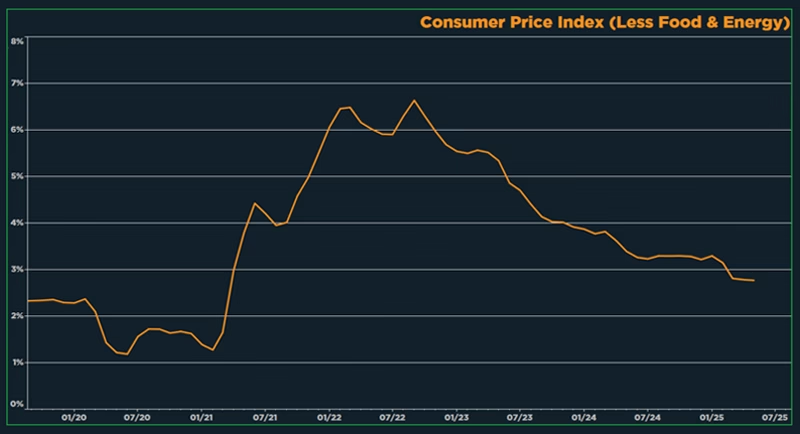

Core CPI, which excludes food and energy, remains north of 2.5%; and has shown little disinflation over the past 12 months. This is a more directionally accurate measure of the impact that monetary and fiscal policy has on prices.

Short term rates have begun to fall in anticipation of:

In our Q1 2025 market forecast we predicted that conflict would emerge between Trump and Powell due to misaligned personal incentives – this has indeed been the case. Trump wants a roaring domestic economy and higher asset prices – a weaker dollar and hot inflation is necessary to facilitate this. Powell wants to go down in history as the ‘Paul Volker’ of this era, rather than the ‘money printer go brr’ meme, of which he became the embodiment of back in 2021. As such Powell is adamant that no further rate cuts are necessary. Lower rates on the front-end of the curve are signaling that Powell’s time as the Fed chair may soon be coming to an end. This is bullish for risk-on assets.

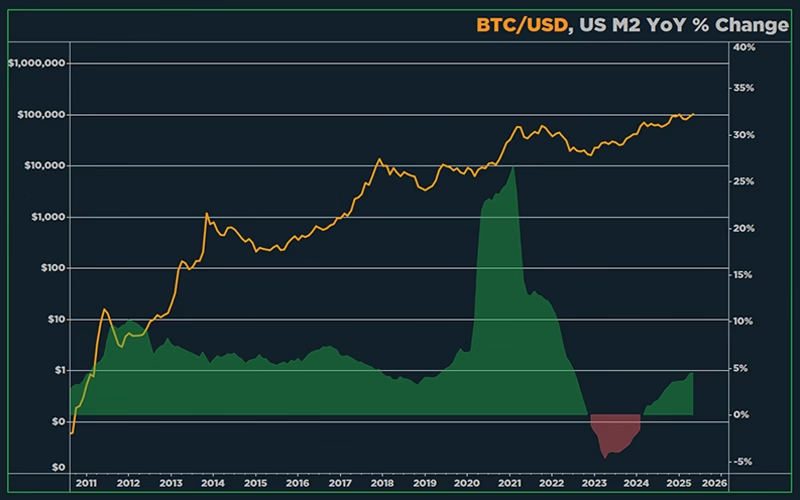

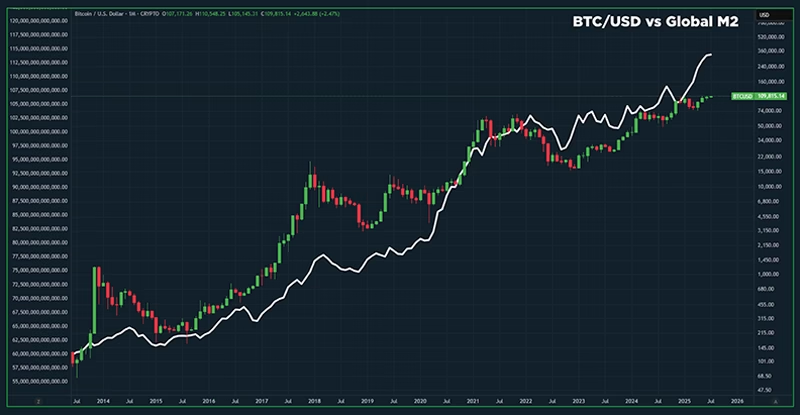

Global liquidity, which is arguably the most important indicator for the Bitcoin price, is increasing across the board. The US M2 money supply is up over 4% YoY and trending higher. While modest compared to pandemic-era extremes, this signals the reversal of the monetary tightening cycle. We’ve exited the “disinflation + contraction” phase and are now in the early stages of monetary re-acceleration. “Higher for longer” interest rates are proving ineffective in limiting the growth of the money supply in the face of relentless fiscal deficits.

Every major Central Bank in the world has begun lowering their policy rate. Despite the Fed’s reluctance to lower the overnight rate in the US, global liquidity is expanding in sync. — an important backdrop for capital rotation into hard assets and high-beta risk.

The U.S. dollar has gotten pummeled this year. The $DXY started the year at 109 and is now to 97. This is an even sharper drop than in 2017, the first year of Trump’s first term, where the $DXY dropped 10 points from 102 to 92.

The weakening of the dollar is partially by design – a weaker dollar supports Trump’s ambition to review the US manufacturing base while also providing tailwinds to asset prices. However, much of the dollar’s decline in 2025 can be attributed to foreign investors shifting capital away from US Treasuries due to tariff policy volatility and long-term fiscal instability.

Demand for US Treasuries is fracturing. Historically, times of uncertainty have resulted in increased demand for U.S. Treasuries. ‘Uncertainty’ has been the dominant theme of 2025, yet we’ve seen the exact opposite. Persistently negative real yields and political risk have forced capital to seek alternatives: gold, foreign equities, and most importantly, Bitcoin. As confidence in sovereign debt erodes, Bitcoin’s profile as a scarce, neutral, borderless reserve asset becomes even more compelling.

The end of the U.S. Treasury supremacy won’t arrive with a bang — it will happen gradually, through capital flight, currency dilution, and the monetization of Bitcoin.

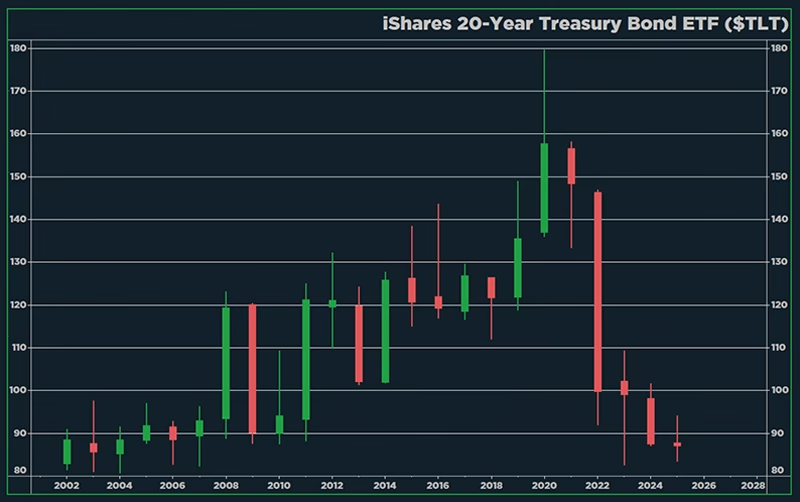

Long Duration US Treasuries are down 1% year-to-date and are on pace for a 5th consecutive year of negative returns.

Bitcoin is now a macro asset. ETF inflows, long-term holder conviction, and increasing strategic buys from public treasuries are driving a new repricing. Here’s our bear, base, and bull case for EOY 2025:

Bear: $110,000

Base: $125,000

Bull: $150,000+

Our short-term price expectations are guided by Bitcoin’s trend since January 2024; the start of the institutional era onset by the creation of US Spot Bitcoin ETFs. During this era Bitcoin has experienced a sequence of rise, consolidation, and rise.

Moreover, our $125,000 base case is derived from the Market Cap to Realized Cap Ratio (MVRV Ratio). During the Bitcoin pumps of Q1 2024 and Q4 2024, the MVRV Ratio reached ~2.7. Based on the current Realized Cap of $959 billion, a 2.7 multiplier would bring Bitcoin’s Market Cap to $2.58 trillion for a BTC price of approximately $125,000.

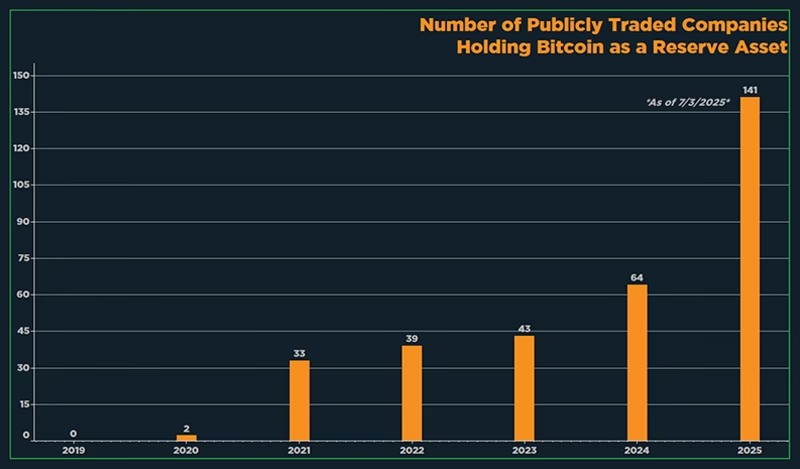

Bitcoin Treasury Companies are the aforementioned ‘bridge’ connecting equity and debt markets to Bitcoin. Thus far in 2025 the number of publicly traded companies with BTC on their balance sheet has increased 120% – from 64 to 141.

This is just the beginning. In the next 6 months, we expect at least three dozen more public companies to add Bitcoin to their treasury. The corporate Bitcoin adoption race is mostly being spearheaded by brand new companies or dying companies you’ve never heard of. This is a feature, not a bug. Companies with struggling core businesses (low growth, dying markets) have a much easier time recognizing the simplicity of investing retained earnings into BTC and earning 40 to 60% CAGR without the operational risks of running a business.

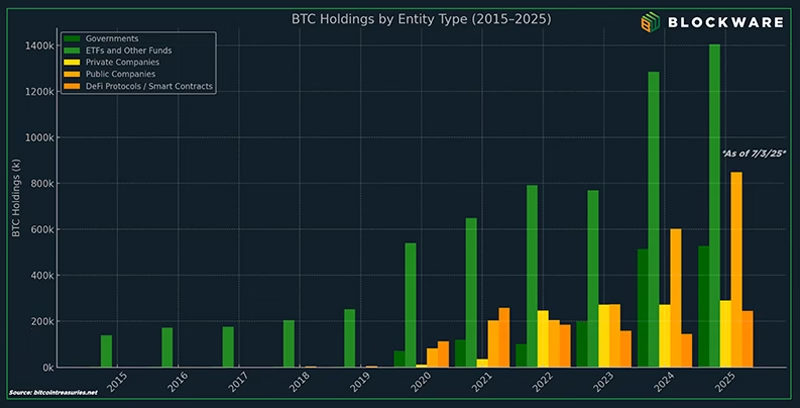

In 2025 BTC Treasury Companies have acquired ~247,000 BTC . For reference, the spot Bitcoin ETFs, which have had the most successful ETF launch in history, have acquired “just” 120,000 BTC year-to-date. The market is sending a strong signal: securitized Bitcoin exposure is here to stay.

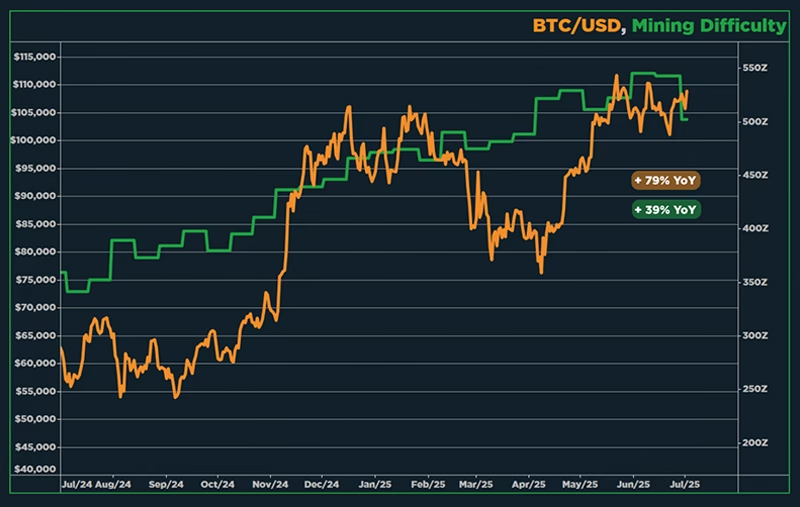

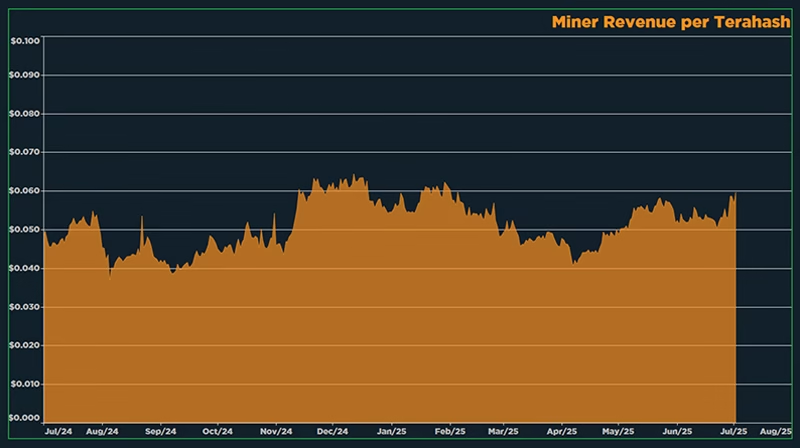

Over the past year the Bitcoin price is up ~73% while mining difficulty is up ~__% – with the net result being an increase in mining profitability. Year-over-year hashprice, the primary metric of mining profitability, is up ~23%. One of our core thesis’ is that the Bitcoin price will increase at a faster rate than mining difficulty between now and the 2028 halving. Why? Simply put: it’s easier to bid BTC than it is to build data centers. This trend will continue the rest of this year and Bitcoin miners will thrive.

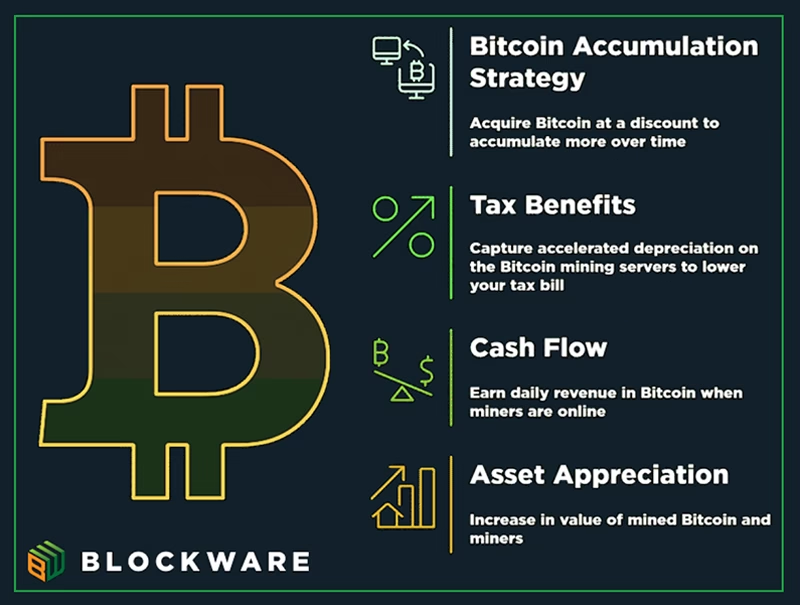

Hosted mining lets you accumulate BTC at a discount, without the overhead of managing a facility or facing import tariffs. Over long periods of time this allows investors to acquire more BTC than they would through a traditional dollar cost average strategy. Moreover, Bitcoin Mining has significant tax advantages. Trump’s “Big Beautiful Bill” renews accelerated deprecation. Meaning that Bitcoin miners will be able to write-off 100% of the cost of their mining hardware in a single tax year.

Blockware’s turnkey model delivers the highest beta exposure to Bitcoin upside, while simultaneously allowing you to accumulate BTC directly to your self-custody.

The macro regime has shifted. Growth is strong, inflation is sticky, liquidity is rising, and Bitcoin is being monetized. Whether you’re an investor, a miner, or a corporate executive, the second half of 2025 offers one of the best asymmetric opportunities in Bitcoin’s history.

Blockware is here to help you capitalize

Contact Us: [email protected]

Start mining today: marketplace.blockwaresolutions.com

Sign up for a free mining consultation: mining.blockwaresolutions.com/consult

Sign up for our newsletter: newsletter.blockwaresolutions.com

Read our previous research: https://www.blockwaresolutions.com/products/research/