An all encompassing retrospective on the 2020 – 2025 Bitcoin halving epoch. If you’re new to Bitcoin and you want to get caught up to speed, or if you’re a Bitcoin veteran and you want to reminisce on the past year’s events, this report has you covered. We break down every notable event in Bitcoin and Macro since the 2020 halving.

I. Introduction

II. 2020

II. 2021

III. 2022

IV. 2023

V. 2025

VII. Conclusion

The 6.25 epoch, spanning from May 11th, 2020 until ~April 19th, 2025, stands as one of the most transformative times in Bitcoin. This epoch was littered with landmark events in which Bitcoin evolved from a niche, cypherpunk hobby, into an asset worthy of inclusion on the balance sheet of nation-states and billion-dollar corporations. This is the epoch in which Bitcoin’s value proposition as a non-sovereign store-of-value, and its potential to disrupt legacy financial markets, became readily apparent.

This research report aims to provide an in-depth retrospective analysis of the major occurrences during this halving epoch; shedding light on the trends, challenges, and milestones that defined this era in Bitcoin history.

Before we get down to brass tacks, let’s take a look at how a few key Bitcoin metrics have grown over the past four years.

By every fundamental metric, the Bitcoin network is light years ahead of where it was at the time of the 2020 halving. The market cap is nearly an order of magnitude higher. The average cost-basis on-chain (realized price) is up 400%. More than five times as much computational power is being used to support the network. The amount of address and activity on-chain has doubled. Coins continue getting swallowed by long-term HODLers. And a nation-state has adopted BTC as legal tender.

Setting the Stage

For the entire world, early 2020 is a time that will never be forgotten. But that especially rings true for those involved in Bitcoin. In the wake of the Covid-19 pandemic, there was a flash crash in which BTC dropped ~50% within two days. Bitcoin wasn’t the only asset to tank, every major US Stock index dropped double digits. Investors rushed to where they felt safest: US Dollars.

This black swan event, which took place just two months prior to the 2020 Bitcoin halving, paved the way for unprecedented monetary expansion, of which its consequences are still impacting the macroeconomic landscape to this day.

Halving and Immediate Aftermath

The rapid monetary expansion, stimulus, and rate cuts began reflecting in asset prices very quickly. By the time the halving rolled around on May 11, 2020, BTC sat at ~$8,600, having recovered all of the losses it experienced from the Covid-19 flash crash. However, it remained well below its December 2017 high of ~$20,000.

The block subsidy dropping from 12.5 BTC to 6.125 BTC was a lethal blow to the weakest Bitcoin miners on the network; those operating with inefficiency ASICs and/or low power costs. Two consecutive negative difficulty adjustments ensued as hashrate dropped from 118 EH/s to 92 EH/s.

Price action wise, the immediate aftermath of the halving was mostly uneventful. BTC traded sideways throughout the summer with no major moves until Q4.

Antminer S19 is Released

Right around the time of the halving, Bitman released the machine that would go on to be the bread-and-butter for Bitcoin miners throughout the epoch: The Antminer S19. The first rendition of the S19 came in at 95 Th/s & 34 W/Th. This ASIC boasted a significant advantage over its predecessor, the S17, which operated at 50 Th/s & 45 W/Th. Following the initial post-halving miner capitulation, hashrate would resume its decade-long up-trend throughout the remainder of 2020.

Bitmain would go on to release multiple variations of the S19 throughout the epoch; the S19j Pro, S19j Pro+, S19K Pro, and S19 XP. One of our latest Blockware Intelligence research reports examines the performance of Bitcoin miners who purchased an S19 upon release. You can read more about that by clicking here.

MicroStrategy Adopts Bitcoin as Primary Treasury Reserve Asset

At the time, Michael Saylor was simply the CEO of a relatively unknown mid-size enterprise software company. Today, Michael Saylor is commonly referred to as “Giga Chad”, and is one of the most beloved members of the Bitcoin community. At the time of writing, his company, MicroStrategy, holds ~214,246 BTC (worth ~$13.7 billion).

On July 28, 2020, Michael Saylor announced in a Microstrategy shareholder meeting that they were considering alternative treasury reserve assets, outside of the US dollar, due to

fears about inflation. Saylor considered multiple different assets, including gold, fine art, and real estate, before ultimately settling on Bitcoin. On August 11, 2020, MicroStrategy officially adopted Bitcoin as its primary treasury reserve asset. They accumulated ~21,454 BTC with an initial allocation of $250 million.

BTC Bull Market Begins – Q4 2020

The start of this cycle’s bull market began in the 4th quarter of 2020, in which Bitcoin posted one of its highest quarterly gains of all time, increasing 176% from $10,600 at the start of October and closing the year at $29,300. After breaking its previous all-time high of $20,000, BTC ripped into the stratosphere, with the effects of loose monetary policy and a halving-induced supply squeeze manifesting in its USD exchange rate.

Bull Market Rages on – Spring 2021

2021 picked up right where 2020 left off, with BTC rallying into undiscovered territory. Knocking off milestone after milestone: $30,000, $40,000, $50,000, $60,000. Alongside the aforementioned catalysts, the accumulation of Bitcoin by the Grayscale Bitcoin Trust, as well as continued accumulation by MicroStrategy, were doing their part to drive the Bitcoin price higher. GBTC began the year with ~57,000 BTC under management. By the end of February, their estimated holdings had reached 661,000. Many GBTC investors were riding high as it held a premium to NAV as high as 38% at the end of 2020

Tell-Tale Signs of Easy Money

Alongside rising asset prices, the effects of the Fed’s loose monetary policy began to materialize in the form of incessant speculation. Look no further than the $GME and $AMC short squeezes. In January 2021, Gamestop and AMC theaters became pawns in a retail-led assault on the short positions of various hedge funds. With their positions being margin-called, short traders were forced to buy the stock to cover their shorts, sending each of these stocks skyrocketing.

Alternative crypto tokens were also riding on the coattails of easy money and the BTC bull run. Dogecoin in particular became one of the only altcoins to ever breach its previous-BTC denominated high. DOGE/USD reached a high of $0.64 before the house of cards came tumbling down.

Normally, we don’t focus our analysis on such superfluous happenings. However, these speculatory events highlight the extreme consequences of the Fed’s policy decisions post-covid. Policy decisions which brought forth record high levels of inflation, across assets and consumer goods. Macro-wise, the entirety of 2022 and 2023 are highlighted by the Fed trying to undo the damage caused by these decisions.

Elon FUD & China Mining Ban Pause Bull Market

The highs of Spring 2021 in Bitcoin and the broader crypto market were realized when Elon Musk appeared on Saturday Night Live to make jokes about dogecoin. At the same time, he pivoted his once-pro Bitcoin stance due to misinformed concerns about its environmental impact; announcing that Tesla would no longer accept BTC as payment for their vehicles.

Around this same time, China banned Bitcoin mining. At the time, a concerning amount of hashrate was located in China. Large-scale Chinese miners were forced to relocate operations elsewhere, or outright capitulate entirely and sell their machines. This had two first-order effects on the Bitcoin market.

These first-order effects are obvious, and they were certainly impactful. But the knock-on effect was equally as important and arguably more interesting. The drop in mining difficulty allowed miners elsewhere to benefit at the expense of the Chinese ban. Mining difficulty dropped nearly 50%, meaning that Bitcoin miners during this time earned 50% more BTC in revenue simply because they were operating in more stable political jurisdictions. Effectively, China shot themselves in the foot by banning Bitcoin as it allowed miners in competing nation-states to accumulate more BTC.

Furthermore, Covid-induced supply chain struggles coupled with a decrease in semiconductor manufacturing resulted in an ASIC supply squeeze, which was compounded by the growing demand for ASICs brought on by the bull market. Antminer S19s, which were ~$2,000 a piece at the time of release, eclipsed $10,000 in late 2020.

El Salvador Adopts Bitcoin as Legal Tender

After announcing their intent to do so at the Miami Bitcoin Conference in June, El Salvador officially made Bitcoin legal tender on September 7th, 2021. Not only did they make BTC legal tender, but El Salvador has begun building a BTC position for themselves. At the time of writing they hold 5,690 BTC, worth ~$36 million. They’ve also since created a plethora of incentives for Bitcoiners and other entrepreneurs to relocate. This is game theory in action.

BTC & Stock Markets Top out in Q4 2021

After the dust from the China mining ban was settled, the bull market resumed in full force. Both BTC and equities were up-only as the abundance of USD-liquidity coursed its way through the veins of the market. Ultimately, the Fed alluding to a hawkish-pivot in the face of rising inflation was a signal to the market, and the point at which the top was reached.

Bitcoin was the fastest horse throughout the tsunami of USD liquidity in 2020 and 2021, greatly outperforming other assets classes. When dollars are rampant in the monetary system, investors look for places to park their capital where it won’t be debased. BTC, with an immutable supply limit of 21,000,000, is the effective choice.

From the point in March 2020 in which the Fed began pumping record-amounts of liquidity into the market, until the peak in Q4 2021, BTC increased by more than 1,000%. Comparatively, the S&P 500 index and NASDAQ 100 posted far less impressive performances

during the same period, +109% & +133% respectively.

Bull Market Begins to Fade

The exuberance of 2021’s price action bled into the early months of 2022, with many investors adamant that bullish price action would resume despite BTC slipping and sliding from its November 8th peak. In retrospect, the abundance of Bitcoin and crypto-related commercials during Super Bowl LVI, an event which gives an unfiltered glance into the state of “normie” / retail culture, was a sign of frothiness in the market. BTC dropped with haste during the months of December and January as forward-looking investors prepared for a hawkish Fed due to rising inflation.

Rising CPI Forces Fed to Tighten Monetary Policy

The effects of the Fed’s loose monetary policy in 2020 first impacted asset prices; as evidenced by the k-shape recovery of BTC and stock indices. The increase in the money supply ultimately manifested as consumer price inflation throughout 2021 and into 2022, with the consumer price index climbing to levels not seen since the 1980s.

The Fed has since effectively admitted that they made a mistake in waiting as long as they did to start raising interest rates. During the early stages of rising CPI, many claimed that “inflation was transitory.” They ultimately did not start raising interest rates until March 2022, by that time CPI had already reached a year-over-year growth rate of nearly 8% (Feb 2022). The effects of monetary policy have a lag, and CPI would continue to rise, peaking in June 2022 at just under 9%.

BTC Begins Dropping in the Wake of Rising Interest Rates

With the Fed firmly hawkish, realization slowly settled in that the music was over, and that $69,000 was in-fact the top for this bull cycle. Bitcoin posted red candles in nine consecutive weeks from March 2022 through May 2022. The tides began to withdraw, and the naked swimmers began getting exposed…

Rehypothecation, Contagion, and Exchange Insolvencies

The first domino to fall was terra, an algorithmic stablecoin supposedly backed by its companion crypto token luna. This led to a contagion of insolvencies across crypto-native investment funds and exchanges. BlockFi, Celsius, Voyager and other rehypothecation exchanges were exposed before the culmination of the contagion when the largest crypto exchange in the world, FTX, went down in November of 2022.

This was a tumultuous time in Bitcoin and the broader crypto market, and it was difficult to keep tabs of all the interconnected exchanges. Here’s a simple flow chart to illustrate the cross pollinated risk

FTX Implosion Set Bottom for BTC

The downfall of FTX ultimately set the floor for BTC, and price began drifting back up shortly thereafter. By January 14, 2022, BTC was back above $20,000. However, broader market sentiment was firmly in disbelief. It should be no surprise that FTX going up in flames set a cycle bottom for BTC; FTX was selling billions of dollars worth of paper BTC.

Several on-chain metrics were screaming bottom-indicators during this time. Long-term holders in the aggregate were holding at a loss, something that has only occurred during the trough of bear markets. Moreover, there was a mass-exodus of BTC off exchanges. The risk of storing BTC with centralized custodians became readily apparent as the dominoes were falling.

Impaired Treasury Bonds Lead to Banking Liquidity Crisis

BTC wasn’t the only asset that entered 2023 looking like a boxer who just got pummeled for five straight rounds, covered in blood and bruises. Stocks and bonds were hammered in 2022 as well. $TLT, the 20+ year treasury bond ETF, entered 2023 down 40% from its 2020 high, and down 27% from the start of 2022.

Banks that used customer deposits to purchase long duration bonds back when yields were below 1% were now significantly underwater (bondyields and bond prices have aninverse relationship). Some of these banks were forced to sell their bonds at a loss in order to meet customer deposits. As concerns around the solvency of major banks spread, a rush for deposits ensued, an event commonly known as a bank run. This exacerbated the problem and resulted in the 4 largest bank failures of all time. Signature bank, first republic

bank, silicon valley bank, and credit suisse all collapsed.

Fed Response – BTFP

With the entire fractional reserve banking system getting exposed, the Federal Reserve had no choice but to intervene in order to prevent broader insolvency in the global banking system. In order to prevent distressed banks from having to sell bonds at a loss, the Fed created a program called BTFP, which stands for the Bank Term Funding Program. This program allowed banks to borrow money from the Fed equal to the par value, rather than the lower market value of the bond.

While BTFP allowed the Fed to stop the banking system from collapsing, the cracks induced by the Fed’s maniacal rate hiking crusade were beginning to show. Moreover, this event was net-positive on liquidity, essentially working against the Fed’s goal of taming inflation. Inflationary forces contrasting the Fed’s rate hikes have become one of the dominant themes in markets during this era, more on that later.

In the wake of the banking crisis, bitcoin ripped from $20k to $30k, a 50% increase, in just a 1 month period. This should come as no surprise as banking insolvencies do a great job of highlighting Bitcoin’s value proposition as a bearer asset with zero counterparty risk.

Fed Continues Raising Interest Rates

The bond market reacted precipitously to the bank failures, with yields plummeting across the board as cash flocked to safety. The 2 year yield dropped from 5% to under 4% in just 3 trading days. However, after the Fed’s May meeting in which Jerome Powell remained firm in his hawkish stance, yields began climbing once again and continued to do so throughout the year. The Fed’s number one objective during this time was to get CPI back to 2% in order to ease the rising political unrest as a result of high inflation, and also to regain credibility with the public.

To date, despite inducing a period of solid disinflation (not to be confused with deflation, disinflation is a period in which prices are rising but at a slowing rate), the Fed has yet to reach their 2% target. And it appears that this could be the new normal, as disinflation has subsided and CPI has hovered around 3% for the past few months.

Ordinal/Inscription Craze Sends On-Chain Bitcoin Fees Soaring

In Q2 2023 we saw on-chain transaction fees reach levels previously seen only during bull market tops. It was discovered that the taproot soft fork effectively allowed users to store various files (text, images, etc.) on-chain by inscribing data to a UTXO. Moreover, users also began creating BRC-20 tokens, using the Bitcoin protocol to trade alternative, speculative crypto assets.

This activity caused on-chain transaction fees to go parabolic for a few periods of time during 2023. These types of activity taking place on-chain is a hotly contested issue. Regardless of where you stand on the issue, you can objectively observe two facts from this:

A conversation ensued within the Bitcoin community regarding the importance of proper UTXO management. You could see on-chain that users began consolidating UTXOs as fees declined; evidenced by a drop in the number of addresses with a non-zero balance. Users consolidate UTXOs by sending various “chunks” of BTC to a single address, in a single transaction. You can learn more about UTXOs by watching this video.

Spot Bitcoin ETF

In Q2/Q3 2023 it was revealed that Blackrock and other financial titans were applying to the SEC to create spot-Bitcoin ETFs; a product that, if allowed, would open the floodgates for institutional capital to gain exposure to spot BTC through traditional financial rails.

The initial response by the market was one of exuberance. BTC ripped from $25k to $30k within a matter of days. However, after the initial excitement wore off, BTC grinded sideways throughout Q3 as questions arose about the timeline of ETF approval, with analysts unsure that approval would happen during that calendar year

Crabbish price action remained the status quo until the fateful Monday morning of October 16th. Cointelegraph falsely reported that the spot ETF had been officially approved and was ready for trading. Within minutes, Bitcoin pumped 10 from $27k to $30k, only to come back down just as fast once word spread that the rumor was false.

However, the market’s response was telling, and soon the inevitability of a spot-ETF, and implications thereof, began to set in. BTC ripped in Q4, closing 2023 at ~$42,000. Total BTC returns in 2023 were ~152%

Spot Bitcoin ETF – Approved

After much anticipation, the spot ETFs were finally approved and began trading on January 11, 2025. Even the biggest ETF bulls were caught off-guard by the speed and potency in which Wall Street embraced these products. Daily inflows to the tune of multiple hundreds of millions of dollars began almost immediately. $IBIT, the Blackrock spot Bitcoin ETF, became the fastest ETF to ever reach $10 billion AUM. To date, the nine new spot Bitcoin ETFs cumulatively hold ~221,000 BTC; worth ~$14 billion.

Grayscale, whose trust was converted to an spot ETF, elected to keep their annual fee at 1.5%, despite competitors offering much lower rates including months-long teasers of 0%. They did so under the expectation that $GBTC holders would be unkeen on rotating into the other products, realizing gains and creating a taxable event. They appear to have been mistaken as GBTC outflows are still occurring at a clip of 10,000+ BTC per week, three months post ETF launch. Initial outflows were north of 10,000 BTC per day. This has placed some sell-pressure on BTC, but most of this capital is returning as buy pressure as it gets rotated into the other ETFs.

New All-Time High

Driven by the influx of capital via the ETFs, into an already illiquid market on the supply-side, BTC, for the first time ever, reached a new-all time high prior to the halving even taking place. BTC has reached as high as ~$74,000, but has since traded sideways between ~$62k and ~$70k. Pull backs of this magnitude are typical for bull markets; the path to global reserve asset status will not occur in a straight line.

Fiscal Dominance

On the macro-side of things, the Fed finds themselves firmly stuck between a rock and a hard place. Decades of budget deficits have brought the US National Debt to almost $35 trillion. Elevated rates in this environment are not having the negative effect on consumer pricing that they allegedly want to see. Interest payments on treasuries yielding 5% are compounding the deficits, resulting in more inflationary pressures. However, lowering interest rates will also be inflationary. Prices remain a key issue at the time of writing, with the Fed unable to bring inflation metrics down to their targets. The market’s outlook has begun shifting from the optimism of May or June 2025 cuts, with “higher for longer” appearing to be the more likely scenario. In the short, medium, and long term, debasement of the US dollar will occur.

In light of this, Bitcoin offers an opt-out from the broken, traditional financial system. With no leader at the helm at an immutable supply limit of 21,000,000, Bitcoin grants property rights to everyone in the world.

By every quantitative measurement, Bitcoin is in a far more mature position now than it was at the beginning of the 6.25 epoch. Moreover, sentiment towards Bitcoin from incumbent institutions of power has become far more favorable:

The song of institutional Bitcoin adoption began in the 6.25 epoch, but the chorus will really hit during the 3.125 epoch. With the financial plumbing in place to allow easy exposure to the asset, and the “Bitcoin is a bubble” narrative effectively deceased in the circles with the most capital, Bitcoin is likely approaching the phase of exponential ‘S-Curve’ growth as a store-of-value.

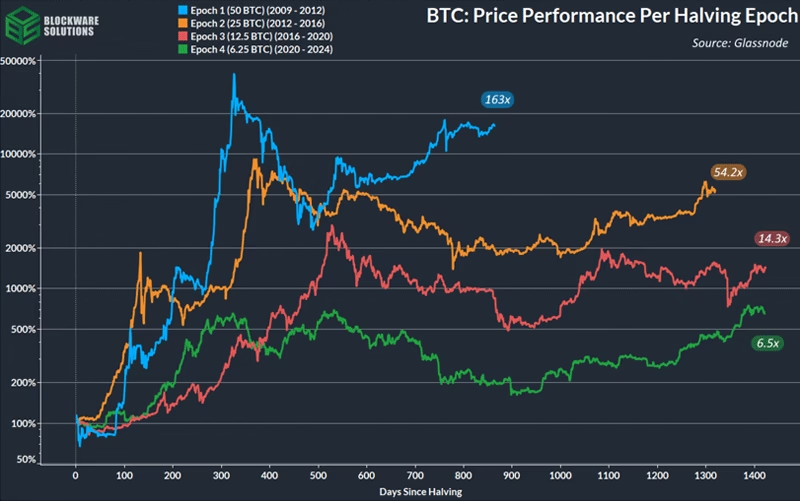

Short-term price action is noise. Each halving epoch results in the purchasing power of BTC growing tremendously; with the 6.25 epoch being no different. The price of BTC increased by ~6.5x since the 2020 halving. Similar growth during this cycle would put BTC at a price of ~$410,000 by the 2028 halving.

Most things in the future are uncertain, but 21,000,000 Bitcoin is not. Blockware Intelligence will continue to provide insights into the dynamics of Bitcoin, Bitcoin Mining, and Macroeconomics. Make sure to subscribe to our newsletter and follow us on X to stay in tune with it all.

All content isfor informational purposes only. This Blockware Intelligence Report is of general nature and does consider or address any individual circumstances and is not investment advice, norshould it be construed in any way astax, accounting, legal, business, financial or regulatory advice. You should seek independent legal and financial advice, including advice asto tax consequences, before making any investment decision.