Bitcoin experienced a difficult 2022, but the outlook for 2023 could be quite different. Read what Blockware Intelligence forecasts from a Macro, Bitcoin, Mining, Energy, and Geopolitics perspective.

Disclaimer: All of the statements below are strictly theoretical predictions. Although data-driven, these hypotheses should not be interpreted as investment advice. Own your own trade.

Due to the fact that we remain in a supply constrained environment in the energy sector, we will continue to see historically-elevated CPI values heading into 2023. Heightened energy prices does incentivize investment from energy companies into expanding current supply capabilities, but this is a time intensive process.

We will, however, most likely continue to see declining year-over-year CPI values. We saw increasing MoM values in August, September, and October, yet this rate of increase is less than that of 1-year ago. For this reason, YoY figures will likely continue to fall, while MoM figures remain heightened.

Just because headline CPI may be declining does not mean that inflation is no longer an issue. Interest rates will be held at heightened levels in 2023 in order to suppress prices, as we’ll examine next.

We have seen increasing MoM values in the energy components of CPI. While this is unlikely to persist throughout the entirety of 2023, it could be the key contributor to high inflation lingering throughout 2023.

Due to elevated prices likely remaining a large issue in 2023, we can expect the Fed to remain contractionary in their policy. In Powell’s November 2nd speech, he stated that a reduction in the size of rate increases is something that will likely see in the upcoming December or February Fed meeting.

As Powell has discussed consistently, the Fed plans to raise interest rates to a “neutral level”, and then hold rates there as long as it takes to lower prices. It appears unlikely that we see the Fed begin lowering interest rates in 2023, but it’s not off the table.

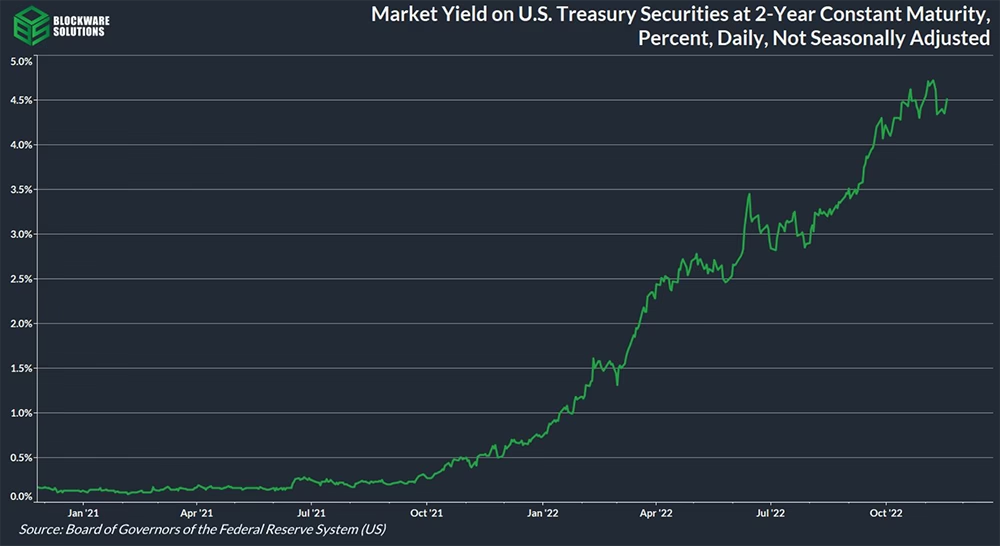

According to current Fed Funds futures data, the derivatives market is currently expecting to see the FFR peak in the range of 5.0-5.25% on the March 22nd meeting. The 2-year Treasury yield is indicating something similar, showing rates peaking around 5.0%. Our team believes it’s possible that the Fed is forced to raise rates higher than 5% if inflation remains sticky in 2023.

The yield of the 2-Year Treasury note is indicating that a Fed terminal rate of 4.5-5.0% is likely to come in the earlier half of 2023. At the time of writing, the 2-Year peaked on November 7th at a closing yield of 4.72%.

In August 2022, we saw the first major decline for home prices since 2011, as measured by the Case-Shiller Index. This comes after a period of aggressively rising mortgage rates. According to Freddie Mac, the average 30-year fixed mortgage rate in the US climbed nearly 4% in 2022, from 3.11% to a peak of 7.08% in November.

If interest rates are held at elevated levels throughout 2023, we can expect to see a continuation of decreased demand for mortgage signings and thus, even lower housing prices.

With interest payments remaining high across the board, we can expect to see a continued strain on gross margins. If this is to persist throughout 2023, it will likely result in an increase to unemployment.

That being said, the US economy has appeared fairly robust in 2022, so we may not see a drastic increase to unemployment.

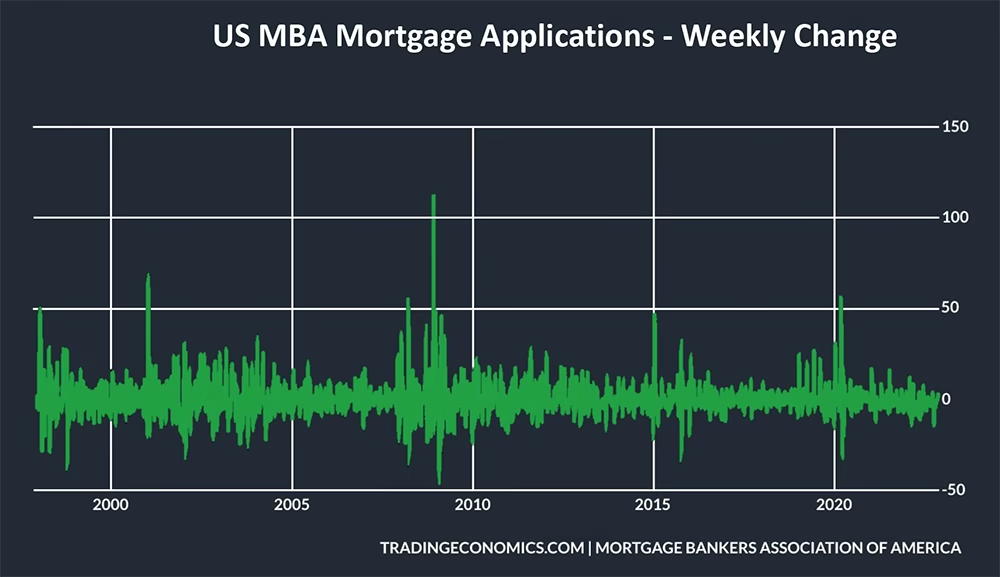

In October 2022, we saw the worst week for new mortgage applications since 2020 at -14.2% for the week of 10/5. While significant, this decline in demand doesn’t compare to 2020, 2016, 2009, or 2000’s destruction of demand. With rates held higher, we can expect to see continued declining demand, and prices, for homes.

Bear markets tend to be much shorter cycles than subsequent bull markets. For this reason, we will likely see the markets bottom in the first half of 2023. At this time, we find it unlikely that markets bottomed in 2022, but it is possible.

The most likely scenario appears to be that prices would bottom at or near an announcement of the Fed that they will be halting the increases to the Fed Funds Rate. The US will likely remain in a declining PMI environment which could push into extreme lows.

This recessionary signal may coincide with extreme drawdowns to the equity indexes. We also may also see the decline in the US’ M2 money supply come to an end in 2023. This increase to market liquidity tends to usher in higher prices for assets and securities.

While prices bottoming are probable in 2023, the extent of the drawdown means that we will likely require an extensive period of sideways price action before heading back higher.

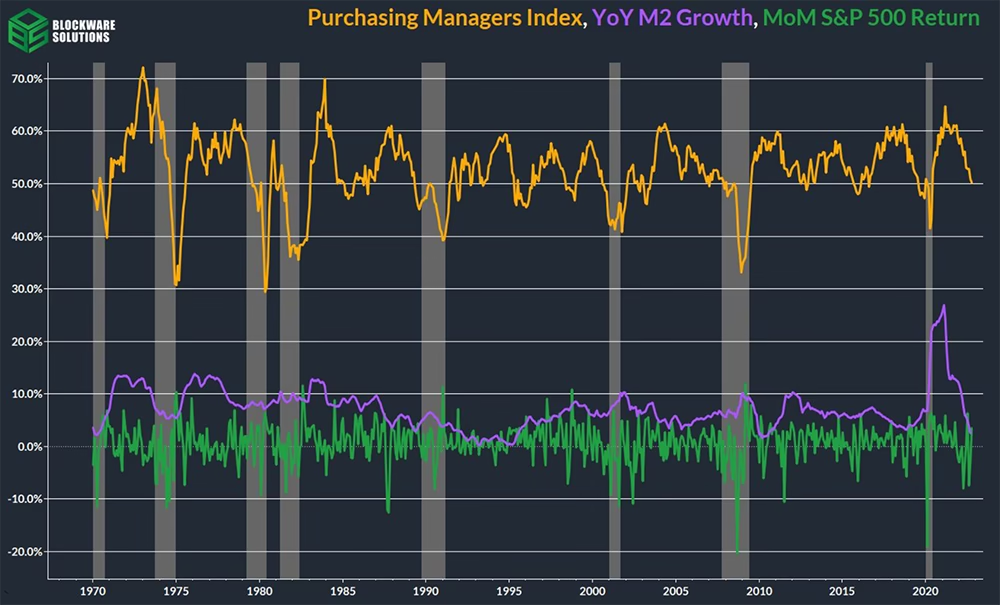

As you can see above, large drawdowns to the Purchasing Managers Index (PMI) below 50 tend to be an accurate recessionary indicator. While a PMI 50 is considered bearish, we tend to see recessions at readings near 40. Large dips to the PMI also tend to coincide with deeply negative MoM returns for the S&P 500, as shown above.

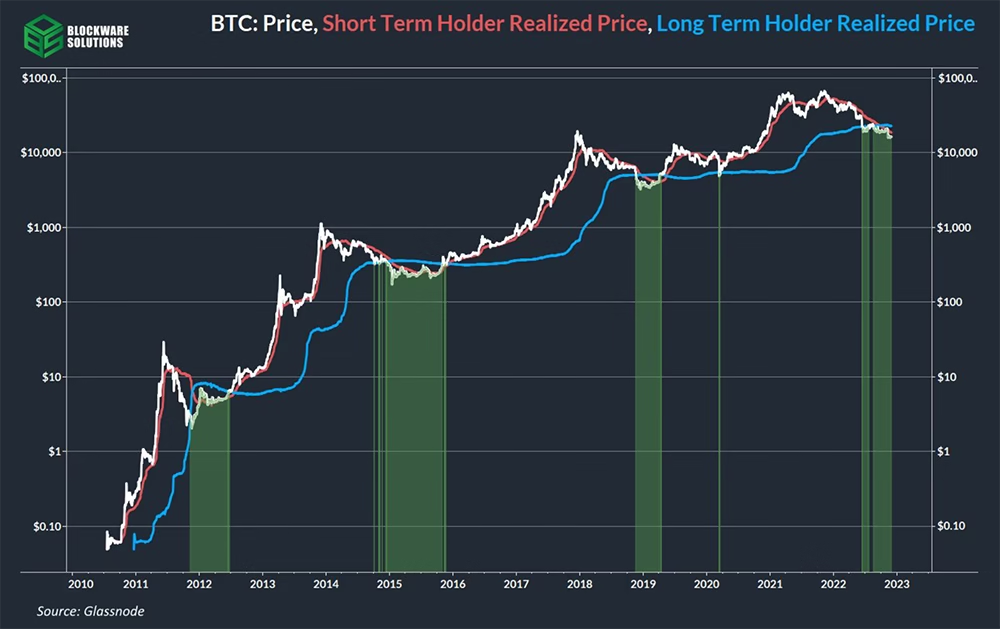

As you can see above, large drawdowns to the Purchasing Managers Index (PMI) below 50 tend to be an accurate recessionary indicator. While a PMI Realized price is a calculation of the aggregate cost-basis of Bitcoin users based on the price of BTC at the time each coin was last moved. Realized price can be broken down into different cohorts based on the holding behavior of on-chain entities; ie. short vs long term holders.

Short-term holder realized price (STH RP) is a salient level of support or resistance during bull or bear markets respectively. During a bull market, short-term holders tend to buy in defense of their cost-basis, and in a bear market short-term holders tend to sell at their cost-basis in order to ‘break even.’ Long-term holder realized price (LTH RP), being far less volatile than STH RP, tends to move sideways for long periods of time with large jumps every bull market due to new market participants, with higher cost-basises, aging into the long-term holder cohort. Price being less than LTH RP is a prominent feature of past bear market bottoms; signaling that, in aggregate, long term holders are underwater.

We anticipate that price will likely flip STH RP and then LTH RP during 2023; signaling the lowest point of the bear market is in.

We forecast that price will likely flip short term holder realized price, and then flip long term holder realized price; signaling that the worst of the bear market is over.

The popular Bitcoin mantra ‘not your keys, not your coins’ became an unfortunate reality for many users storing their funds on exchanges. Virtual bank runs uncovered the insolvency of popular exchanges such as Celsius, BlockFi, and FTX. In an attempt to generate yield, exchanges partook in reckless trading with user deposits, ultimately losing the funds. Contagion ensued and many players in the industry were revealed to have exposure to the insolvent entities.

These insolvencies resulted in large swaths of users withdrawing BTC from the exchanges into wallets for which they posses the private keys; embracing one of Bitcoin’s primary value propositions: ownership of an asset without reliance on a counterparty.

Self-custody is necessary for long term appreciation in the price of BTC. Price suppression occurs when BTC is left on exchanges as exchanges can sell more BTC than they actually have in their possession.

The amount of BTC on exchanges is down nearly 1,000,000 since it’s peak in 2020. Declining exchange balances will likely be a prominent theme in 2023.

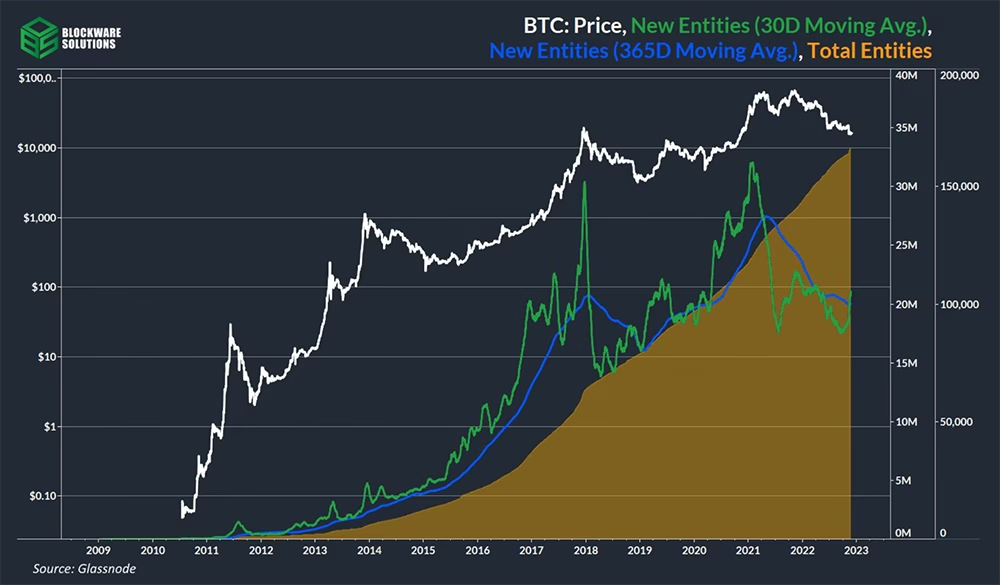

In June 2022 we published the Bitcoin User Adoption Report. The thesis of that report was that Bitcoin is still in the early stages of the ‘S-Curve’ that the adoption of disruptive technologies tends to follow.

As more people are educated on the value proposition of Bitcoin, an immutably scarce monetary good with zero counterparty risk, it’s adoption rate increases. This is evident by the growing number of on-chain entities. While the growth rate is always positive, it tends to accelerate during Bitcoin bull markets. Right now we are seeing the start of that acceleration indicated by the 30D moving average of new entities crossing above the 365D moving average. This positive momentum reversal of new entities occurred at the bottom of the 2018 bear market and will likely ignite the next bull run.

As uncertainty in traditional financial markets continues to persist, the certainty provided by Bitcoin’s immutable and verifiable supply schedule is becoming increasingly appealing to institutional and retail investors alike. We anticipate that the number of on-chain entities will increase significantly in 2023.

We expect the number of on-chain entities to experience a material increase in 2023 as Bitcoin adoption nears the exponential growth stage of the ‘S-Curve.’

The rig efficiency (J/TH) growth rate is slowing due to chip producers approaching the limit of what is thermodynamically viable with modern technology. Today’s premier Bitcoin ASIC, the S19XP, has an efficiency of 21.5 J/TH. The S19XP has transistors the size of 5 nm. For comparison, a human hair is 100,000 nm wide. Viewing each transistor on an S19XP would not be visible to the human eye or even on most microscopes.

The ability to produce ASIC models multiples more efficient in a short period of time is gone. The S19XP will likely be a competitive machine for years to come.

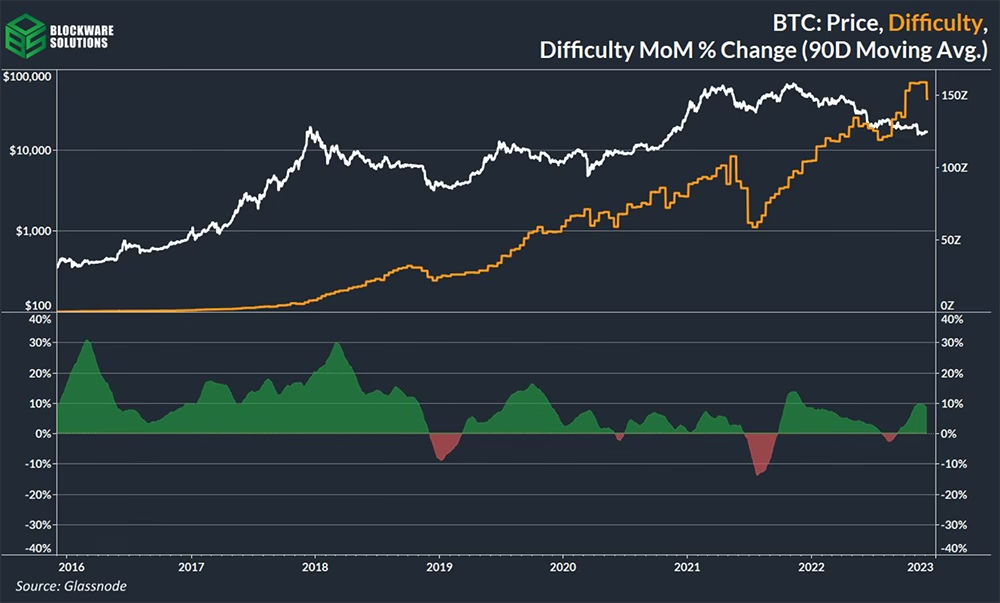

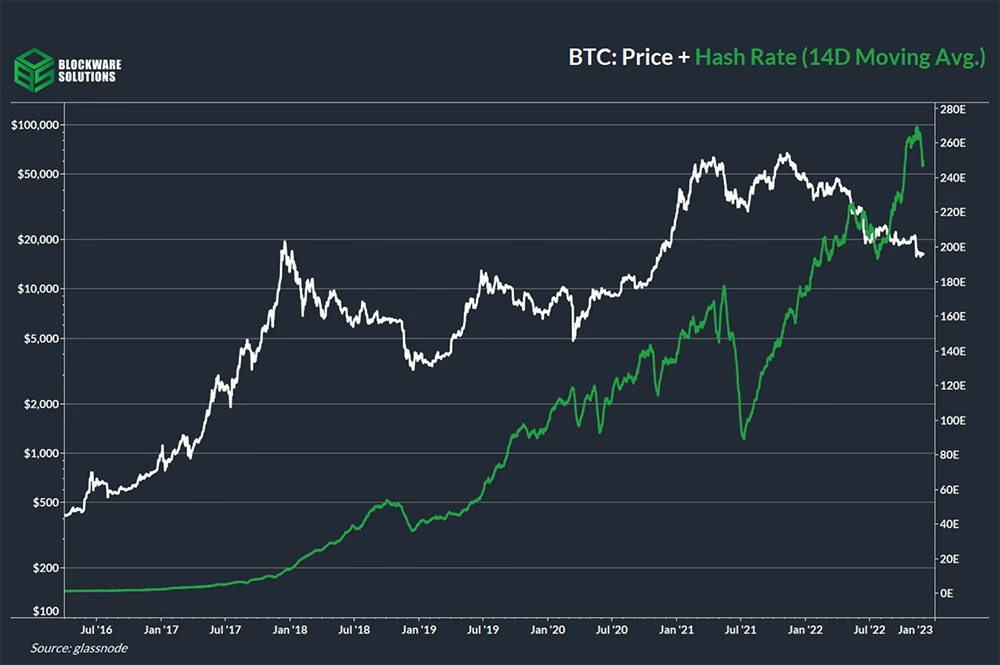

Bitcoin mining difficulty and total network hashrate are correlated 1:1. If hash rate doubles, then mining difficulty doubles. Since ASICs are commoditizing, it is becoming more and more difficult to increase the network hash rate by manufacturing a new advanced ASIC. Instead, hash rate and difficulty are growing due to increased consumption of cheap and wasted energy.

2023 will likely be a slow year for global hashrate growth because of three key factors.

Mining rigs and infrastructure cannot be built overnight. If BTC 10x’s to $200k, after the next halving, then 44 GW of new energy needs to be consumed by the Bitcoin network in order to keep hashprice the same. For comparison, the average electricity production of Mexico in 2021 was 40 GW.

Difficulty growth will continue to slow in 2023 giving the surviving miners some breathing room before the next bull run.

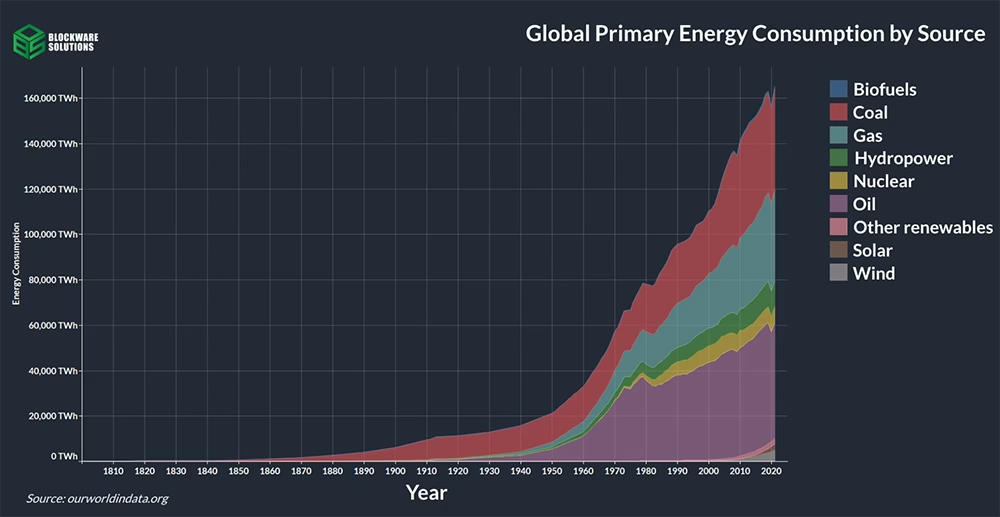

The global supply of energy will likely continue to be unstable. Hydrocarbons (oil & gas) enabled humans to scale economically, but unrealistic regulation hinder their growth.

As the growth of O&G production continues to be blocked by regulators, energy prices will likely remain high as bureaucrats attempt to solve a lack of energy with more wind and solar power, which have proved to be an unreliable source of base load energy. Between 2011 and 2021, oil and gas exploration investments declined by 50%. This lack of base load supply will result in energy prices remaining elevated. High energy prices will prevent new miners from building out infrastructure, securing competitive PPAs, and deploying more capital into BTC mining.

Miners with fixed PPAs and hosting contracts will benefit from locking in low energy rates in an inflationary environment. These miners have effectively secured the cost side of their operations while their revenue will likely grow over time.

Hydrocarbons have enabled massive economic growth since the early 1900s, but recent policies have pushed away from oil & gas and hindered real progress.

Other than the Federal Reserve, the BoJ, ECB, and BoE have already or are likely on the cusp of pivoting to a more accommodative monetary policy. Countries and their central banks will soon be competing again to devalue their currencies relative to their neighboring countries in order to stimulate domestic economic growth. This will positively influence the price of BTC as more liquidity is pumped into global markets.

Of all global fiat currencies, the USD is the strongest and will continue to be so due to the Federal Reserve being in the strongest position to fight inflation. Inflation will likely be felt more outside the United States. The United States is also a net energy exporter and remains energy independent. Energy prices in the US are likely to be more stable compared to net energy importers like most of Europe.

With more stable energy prices and the least amount of inflation, it’s likely that the United States will continue to be the best jurisdiction for Bitcoin mining.

The United States will likely continue to see an increase in the total share of network hashrate. 45% of the total network hashrate may exist in the US by the end of 2023.

When most think of getting exposure to Bitcoin, they rarely think about mining Bitcoin. Mining Bitcoin with a trusted partner like Blockware Solutions enables you dollar cost average into BTC at a discount.

There are two major trends that have fundamentally altered the market dynamics of the Bitcoin mining industry. First, Bitcoin ASIC efficiency improvements for new generation machines are slowing drastically. This means the next-gen hardware does not immediately make the previous-gen hardware obsolete, allowing today’s hardware to retain its value for a longer period of time.

Second, Bitcoin’s network hashrate and the number of rigs hashing continue to grow over time which has forced a large secondary rig trading market to emerge. This means there is now more liquidity for used mining rigs, enabling mining rigs to be purchased and sold at a later date.

ASICs are commoditizing, which means today’s hardware is likely to retain its value for a longer period of time.

There is now more liquidity for used mining rigs, enabling mining rigs to be purchased and sold at a later date.

Blockware Solutions LLC 3800 N. Lamar Blvd.,

Suite 200 Austin, TX 78756