Crypto mining sounds like high-tech wizardry but it drives the backbone of the blockchain world. Most people zero in on the coins as the biggest prize and miss what matters. The IRS treats every mined coin as taxable income the moment you earn it, no exceptions. This shifts crypto mining from a digital treasure hunt to a real-world financial puzzle that every miner needs to solve.

Crypto mining represents a fundamental process in the blockchain ecosystem that goes far beyond simple digital currency generation. At its core, mining is a complex computational mechanism that serves multiple critical functions in maintaining cryptocurrency networks like Bitcoin.

Cryptomining involves solving intricate mathematical problems using specialized computer hardware. Miners compete to validate and add new transaction blocks to the blockchain, essentially acting as decentralized auditors who confirm the legitimacy of cryptocurrency transactions. When miners successfully solve these cryptographic puzzles, they are rewarded with newly minted cryptocurrency tokens, creating an economic incentive for maintaining network security.

According to the United States Internal Revenue Service, crypto mining generates taxable income through these computational rewards. The process is not just about earning digital currency but serves several essential network functions:

Mining represents more than a technical process. It is a sophisticated economic model that democratizes currency creation and maintains blockchain network integrity. By requiring significant computational power and energy investment, mining creates a robust barrier against fraudulent activities. Miners must invest in expensive hardware and manage substantial electricity costs, which naturally discourages malicious network manipulation.

For those interested in understanding the practical aspects of getting started, learn more about crypto mining strategies that can help newcomers navigate this complex landscape. The mining ecosystem continues to evolve, reflecting broader technological and economic transformations in digital finance.

Cryptocurrency mining introduces a complex tax landscape that requires miners to carefully navigate reporting requirements and potential financial obligations. The Internal Revenue Service treats cryptocurrency earned through mining as taxable income, creating significant compliance responsibilities for digital asset participants.

When miners successfully validate blockchain transactions and receive cryptocurrency rewards, the IRS mandates immediate income recognition at the fair market value of the digital assets at the time of receipt. This means miners must track and report the precise dollar value of cryptocurrency earned on the day each mining reward is generated.

According to the Internal Revenue Service, cryptocurrency mining rewards are treated as ordinary income and must be reported on federal tax returns. Key considerations for miners include:

Miners can offset their cryptocurrency mining income by deducting legitimate business expenses related to their mining operations. These deductions might include specialized computer hardware, electricity costs, cooling equipment, and workspace dedicated to mining activities. Proper documentation becomes crucial in substantiating these expense claims during potential tax audits.

For miners seeking to understand the intricate details of cryptocurrency taxation, explore our comprehensive mining tax guide that breaks down complex reporting requirements. The evolving regulatory landscape demands ongoing education and proactive financial planning for cryptocurrency miners.

Reporting cryptocurrency mining income requires precise documentation and understanding of complex tax regulations. Miners must navigate a nuanced landscape of financial reporting that demands meticulous record-keeping and strategic financial planning.

Cryptocurrency mining rewards are classified as ordinary income by tax authorities, requiring miners to report the fair market value of their digital assets at the time of receipt. This means every mining transaction must be documented with its corresponding dollar value, creating a comprehensive financial trail for tax purposes.

According to the Internal Revenue Service, miners must report their cryptocurrency earnings through specific tax documentation methods. Critical reporting requirements include:

Miners can potentially reduce their tax liability by documenting legitimate business expenses directly related to their mining operations. Deductible expenses may include specialized computer hardware, electricity costs, cooling systems, and dedicated workspace investments. These deductions can significantly offset the taxable income generated through cryptocurrency mining.

Discover advanced mining tax strategies that can help miners optimize their financial reporting and minimize potential tax burdens. The evolving regulatory environment demands continuous education and proactive financial management for cryptocurrency mining participants.

Understanding the complex financial landscape of cryptocurrency mining requires a sophisticated approach to tax reporting, particularly regarding capital gains, losses, and potential deductions. Miners must navigate intricate regulations that transform digital asset generation into precise financial calculations.

Cryptocurrency mining introduces unique challenges in tracking financial transactions. When miners receive digital assets as rewards, they must record the fair market value at the time of receipt. Future transactions involving these mined assets can trigger capital gains or losses depending on the difference between the original acquisition value and the selling price.

According to the Internal Revenue Service, miners must carefully document their cryptocurrency transactions to accurately report potential financial implications. Key considerations include:

Cryptocurrency miners can potentially offset their tax liability by documenting legitimate business expenses directly related to their mining infrastructure. Substantial deductions may include specialized computer hardware, electricity consumption, cooling system investments, and dedicated workspace costs. These strategic deductions can significantly reduce the overall tax burden for professional and serious mining participants.

Explore comprehensive mining investment strategies that can help optimize your financial approach to cryptocurrency mining. Proactive financial planning and thorough documentation remain critical in managing the complex tax landscape of digital asset generation.

Navigating the tax landscape of cryptocurrency mining requires strategic planning and meticulous documentation. Miners must understand the nuanced requirements that transform their digital asset generation into precise financial reporting obligations.

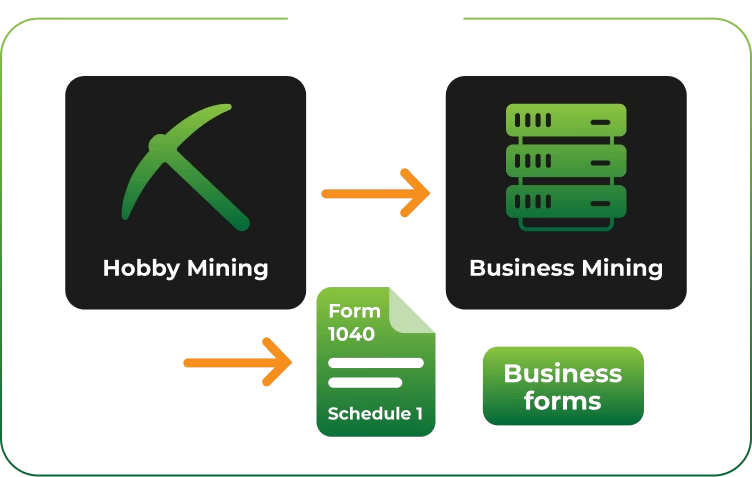

The tax treatment of cryptocurrency mining varies significantly depending on whether an individual is classified as a hobbyist or a professional business operator. Hobby miners typically report their mining income on Form 1040 Schedule 1, while business miners can leverage more extensive tax reporting mechanisms and potential deductions.

According to the Internal Revenue Service, miners must carefully distinguish their operational status. Critical considerations include:

Successful tax compliance for cryptocurrency miners hinges on comprehensive and organized financial documentation. Miners should maintain detailed records including transaction timestamps, fair market values, mining equipment expenses, electricity costs, and any additional operational expenditures. These meticulous records serve as critical evidence during potential tax audits and help substantiate deduction claims.

Uncover advanced mining documentation techniques that can streamline your financial reporting process. The evolving regulatory environment demands proactive approaches to managing the complex intersection of digital asset generation and tax obligations.

If you are feeling overwhelmed by the complexity of crypto mining taxes, you are not alone. The need to constantly track fair market values, manage deductions for mining expenses, and separate hobby from business activities can turn even the most passionate miner cautious. Getting it right is not just about following IRS rules; it is about protecting your hard work and maximizing your profits.

Blockware Solutions is ready to help you break through these barriers. With our expert-hosted mining services, dedicated support, and research resources, you will gain the education and turnkey tools needed to mine smarter and stay tax compliant. Do not let tough regulations hold you back. Visit Blockware Solutions and start building a mining operation that is both efficient and audit-ready. The right guidance makes all the difference—seize your advantage now.

What is crypto mining and how does it work?

Crypto mining is the process of solving complex mathematical problems to validate and add transaction blocks to a blockchain. Miners compete to maintain network integrity and security, and they are rewarded with newly minted cryptocurrency tokens for their efforts.

How are cryptocurrency mining rewards taxed?

Cryptocurrency mining rewards are considered taxable income by the IRS. Miners must report the fair market value of the cryptocurrency earned at the time of receipt on their federal tax returns, typically using Form 1040 Schedule 1.

What expenses can cryptocurrency miners deduct for tax purposes?

Miners can deduct legitimate business expenses such as specialized hardware, electricity costs, cooling systems, and workspace dedicated to mining activities. Proper documentation is crucial to substantiate these deductions.

How can miners calculate capital gains or losses on mined cryptocurrency?

Miners must track the fair market value of mined cryptocurrency at the time of receipt and compare it to the selling price during future transactions. This difference will determine if there is a capital gain or loss, impacted by holding periods and asset classification.